Before I get into a review of my holdings and performance, let's do a little housekeeping. On June 25th, I withdrew $10,000 from my account. This is shown on the "My Returns So Far" page (link to the right) and is also reflected in all the quarter-end exhibits further down.

Additionally, as I'm typing, it occurs to me that I haven't written a new post since April (when I sold my AIG warrants), so I apologize for the lack of activity. It's not that I haven't been thinking about investing, it's just that I haven't had anything especially insightful to say or do. It's also worth mentioning that the AIG transaction took me to roughly 45% cash, and given the recent market decline, the timing couldn't have been better. In fact, in my April post I lamented, "with the overall market close to it's 52-week high, I thought now may be a good time to raise some cash for the next rainy day."

Alright, now let's get to the good stuff.

- I came into the year with $138,179. At the end of Q1 I had $246,569, and I finished Q2 with $206,988. Had I not withdrawn the $10K, I would've finished the quarter with $216,988.

- Although I went backward in Q2, the good news is I'm still way ahead of the S&P for the year. In fact, for the first six months I'm up roughly 57%, whereas the S&P is only up 9%.

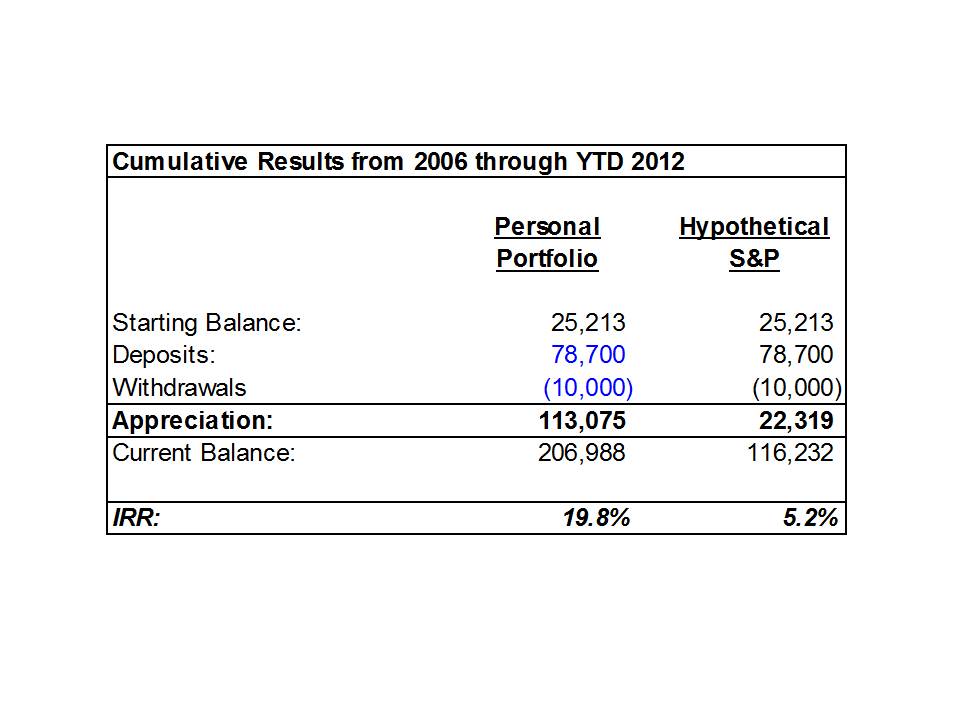

Below are the following exhibits: 6+ year performance summary, waterfall graph, holdings summary, and quarter-to-quarter bridge (all values are as-of 6/30/2012, click to enlarge).

I remain as comfortable as ever with my current holdings (BAC, JEF, LUK, and SHLD). In fact, given the market's recent pullback, I think all of them represent pretty compelling values. Even more importantly, they're all run by fantastic leaders who are focused on building shareholder value.

BAC continues to strengthen their balance sheet and has made significant progress with their back-to-basics business transformation. In the not-to-distant future, they should be allowed to start returning cash to shareholders via dividends and buybacks. In Moynihan we trust!

As CEO Handler says about JEF, "We are the nicest property in a devastated neighborhood." Well I guess that's one way to put it! The fact is JEF operates in what could be a pretty attractive industry. Unlike their peers (Goldman Sachs, Morgan Stanley, etc.), JEF has used the recent economic turmoil to hire talent and make acquisitions on the cheap. Over the next few years, I think we'll see significant earnings growth as these investments start to pay off.

I don't have a whole lot to say about LUK. I'm not thrilled that their Chairman, Ian Cumming, has indicated that he doesn't plan on renewing his employment contract in 2015. However, I am confident that LUK leadership will continue to faithfully build wealth for their shareholders, and I'm curious see what Justin Wheeler (the new COO) can accomplish in his expanded role.

And of course there's SHLD. I've written about this one ad nauseum, so I'm going to keep it short. However, to even the passive observer, it's clear the transformation has begun. So, even if you're not a shareholder I'd keep an eye on this one, things could get interesting.

And finally, let's talk about what's next. Given my high cash %, I'm looking to put some money to work. However, I find myself struggling to actually pull the trigger (which is nothing new). Part of it's the hope that stocks will get cheaper. The other issue is that I've found a handful of opportunities that are pretty compelling, but I'm having trouble deciding which 1 or 2 to buy. Here's what I'm looking at most closely: CNQ, VRX, JCP, SCHW, EXPD, SD, XCO, and AIG. Interestingly enough, I've previously owned JCP, SD, and AIG. If anyone has researched any of these companies, feel free to share!

Questions? Comments? Email mevsemt@gmail.com